Moore, Gilder, and the fading logic of constraint

Moore's Law told us technology gets cheaper. Gilder told us networks grow forever. So what happens to orthodox economics when scarcity stops being the point? A look at digital networks, network effects, and why consumer attention is the only constraint left.

Considering the reversal of economic ‘scarcity’ in the world of digital networks

Gordon Moore and George Gilder are familiar names for proponents of technological development. Respectively, Moore and Gilder conceived theories of sustained exponential growth in the fields of network bandwidth, and semiconductors. George Gilder famously predicted that the world’s total supply of bandwidth would double every six months, and would therefore lead to a profound eruption in our capacity to share knowledge and power. The optimism of Gilder’s hypothesis has certainly been realised — it is virtually impossible to overstate the impact of networked technologies in our lives.

Gordon Moore, Gilder’s theoretical predecessor is held in even higher esteem, ‘Moore’s Law’ is biblical to Silicon Valley’s avant-garde. Through the years, Moore’s famous dictum— an exponential function — has provided the economic basis that has road-mapped some of our greatest inventions — from the mainframe, to the personal computer, to the smartphone.

Moore’s core observation is that the number of transistors on integrated circuits tend to double every 18 months. That Moore’s observation, first acknowledged in 1965, has held true over the ensuing decades is a testament to engineering. It has served as a guiding light for the long-term planning and research and development of technology industries, and its premise has been extrapolated to define the general trend of exponential technology improvement. In 1965, Gordon Moore gave us the means to predict IoT — today’s technology shouldn’t really amaze us at all.

But what’s just as important as the law of exponential growth is its complement: technology’s unrelenting march to the asymptotic ‘free’. As technological capacity doubles in a period, the cost of an equivalent capacity necessarily halves. The essential insight here is that base level technological commodities are constantly approaching the point of ‘nearly free’. It’s a tough logic to consider, but the growth in the availability of computer technologies speaks for itself. The computing capabilities that were once labelled as ‘emerging technologies’ are now tacked onto appliances as trivial as refrigerators and shipping containers, and phones once lauded as breakthroughs are now given away free on contract. The only reason we keep paying for things is because our our expectations grow just as fast as technology becomes cheaper. Lifestyle creep at its macroeconomic finest.

But this story isn’t to deride the tenets of consumerism. Really, this is about considering a new grasp of economics in a world where the scarcity that forces economic agents to make choices is constantly threatened. Digital technology has no desire to be scarce. Digital commodities are naturally anarchic, with a natural propensity to be sharded, scattered, and duplicated. It’s a romantic battle: bits and bytes breaking free from the tenacious bounds of orthodox economics. Chaos is its natural state.

Orthodox Economics

Orthodox economics is foundationally the study of making the right choices. The definition of ‘right’ in economics is a quantifiable matter, usually that which provides us the most monetary wealth or prosperity. The mandate to make choices — a friendly word for trade-offs and sacrifices — is driven by scarcity and opportunity cost. Simply, in a world where we can’t have everything, the best thing we can do is to make choices where opportunity costs are minimised.

There are various ‘schools’ of economic thought that sit underneath this, but they are broadly answers to this same question — how do we best make the choices to generate the most prosperity. Additionally, although a distinction is made between microeconomics (the behaviours of individual economic agents), and macroeconomics (the study of societal welfare), the managerial strategies are often similar.

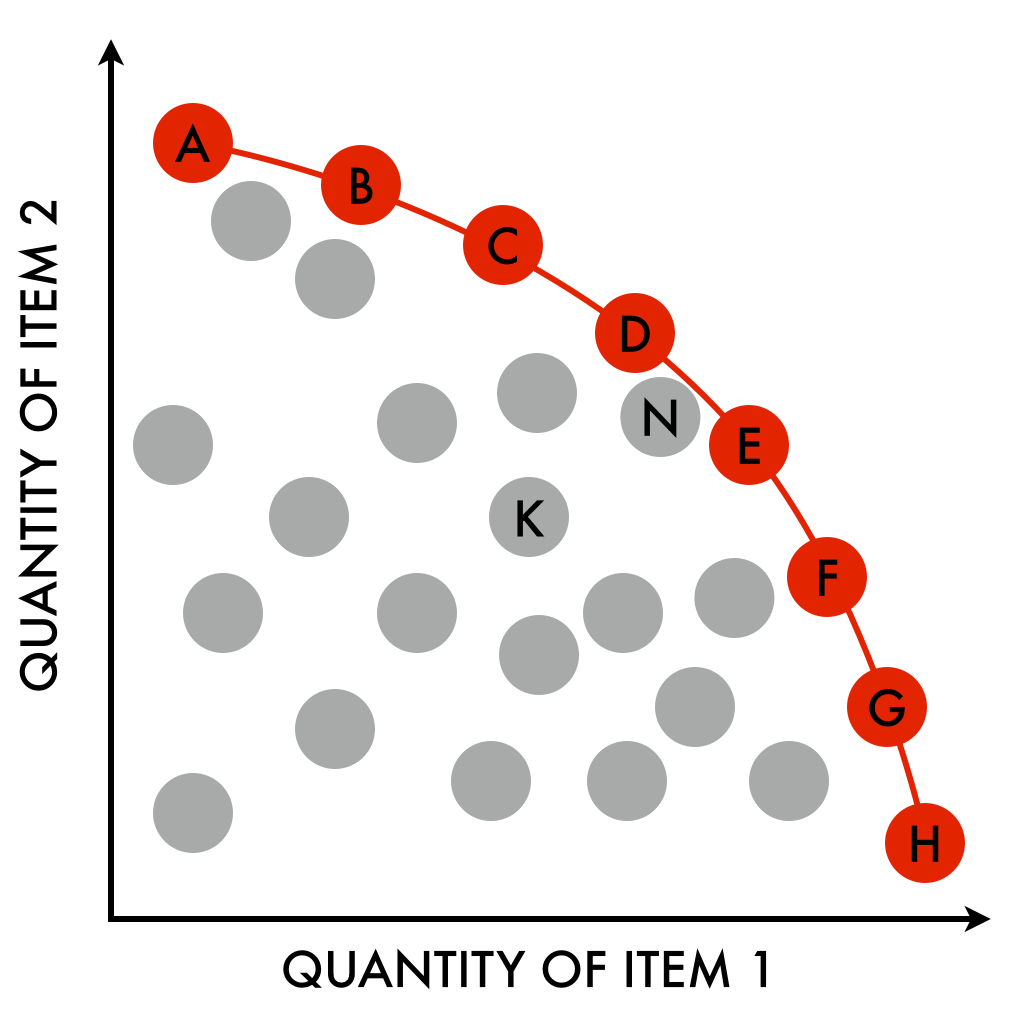

What makes an economy successful in international trade is generally translatable to what makes firms successful within their industries. That is, we prioritise production in areas where we have comparative advantage, trading off production of a next best alternative. Our production choices can be modelled theoretically on a frontier, where we strive for a Pareto-efficient outcome in which resources are fully utilised and production of one good can only be increased at the expense of another.

Generally, the forebearer of these economic choices are governed by aspects in the realm of strategic management. Resource analysis determines the competencies of unique economic players which can be leveraged. For example a vehicle manufacturer with accumulated brand value, specialised manufacturing facilities, and a fertile R+D capability is likely to recognise a comparative advantage in producing high-performance, luxury vehicles. Subsequently, natural production constraints will force a decision on what combination of luxury vehicles to make: 20 sedans and 10 trucks, or 10 sedans and 15 trucks?

Alternatively, a chosen strategy can also influence the resources a firm wishes to accumulate. If a high volume, cost leadership approach is favoured then standardising production components and minimising marginal costs are worthy ‘resources’ to accumulate. The natural trade-off tends to be that the ‘resources’ required to engage a Cost Leadership strategy, are very different to those required for Differentiation or Focused strategies. As such, many economic agents prosper in a given industry by virtue of satisfying niches.

In economics, scarcity rears its head in almost all facets of our understanding of it. It is of course, the core reason to think about economics at all. Generic strategies and the theory of comparative advantage are products of choice. Because we have scarce resources — a resource being anything from manufacturing facilities to brand equity— we have to be selective on how we get the most out of them. Our brand permissions may only provide us with access to a target segment, or our manufacturing capacity may preclude us from being ‘mass market’.

In management, this consciousness of our internal capacity is called a ‘resource-based view (RBV)’. In the parlance of economics we might call this an internal constraint. The key insight then, is that scarcity is an internal affliction, an output of our own incapacity.

Techno-Optimism and the Growth of Networks

Moore’s law and Gilder’s law are products within a larger genus — of techno-optimism, and perpetual progress. Of course, these aren’t natural laws. There exists no organic mandate that guarantees the doubling of microchip power over a two year period other than our willingness and determination to engineer. This belief in our ingenuity breeds a fervent optimism in the powers of us, and of technology. The romance of digital networks is a utopia where ideas and power are shared infinitely, and knowledge has the bandwidth to run free. George Gilder liked to call this the ‘telecosm’, something from a higher order, unblemished in its profundity.

Gilder’s techno-optimism stems from a belief that technology is capable of solving the macro issues that we unsuccessfully try to solve ourselves through all manners of manual intervention. Throughout his life he has been an advocate for Laissez-fairre supply-side economics, and the promises of the ‘telecosm’ have continued to ignite this infatuation with a utopian, post-regulatory society.

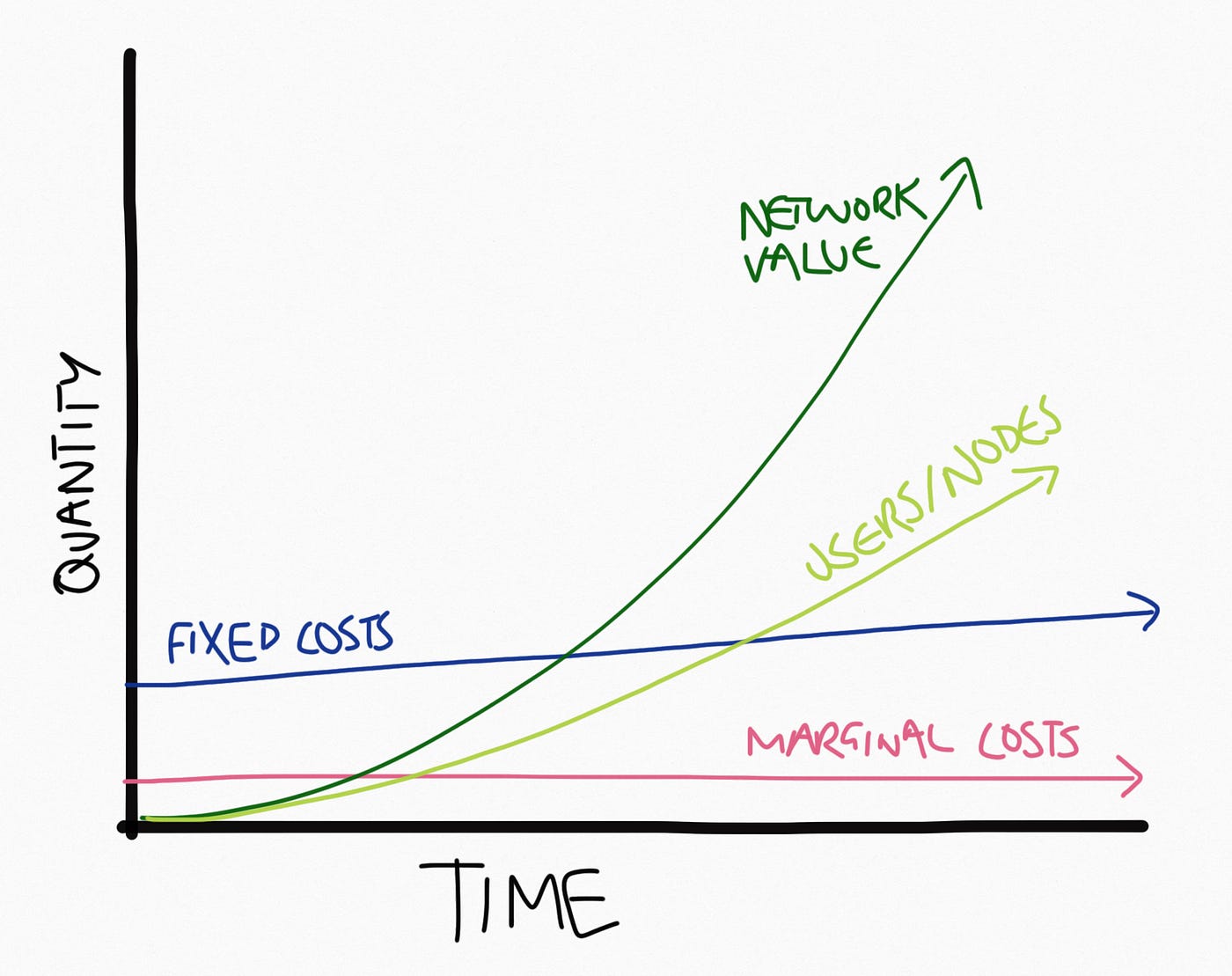

What’s remarkable is that in an academic sense, Gilder’s beliefs have been largely vindicated. Digital networks and digital commodities have continued to advance the notion of the asymptotic free. As more participants join digital networks and are empowered with the tools to engage in our digital economy, digital commodities — thoughts, communication, connections, commerce, information — become more abundant. This abundance in bandwidth is in itself a proponent of supply-side economics. Unregulated digital production has resulted in a literal glut in digital value. With effectively zero marginal costs to create and disseminate digital commodities, scarcity ceases to exist and consumers benefit.

Importantly, we shouldn’t expect this growth to slow down. Because even if Moore’s Law is a mere product of human ingenuity, Metcalfe’s Law — the law of network effects — is natural. The value of a network is proportional to the square of the number of nodes, as a network grows, the value of being connected to it grows exponentially. By sidestepping the natural scarcity of orthodox economics, we have defaulted prosperity. Prosperity is a natural state.

Digital Economics

So what does this mean in the context of orthodox economics? Within digital networks, the theories of comparative advantage, pareto optimality, and even the application of generic strategies may need to be rewired. Put simply, when resources aren’t scarce and trade-offs no longer have to be made, what models do we have left to define optimality or efficiency?

In Monopoly Economy, I covered a necessary side effect of ‘marketplace’ business models which leverage network effects to intermediate exchange between multiple parties. That side effect, is that these businesses are at their best when they monopolise. A large number of Silicon Valley’s ‘unicorns’ adopt this exact business model: Uber connects riders to drivers, Facebook connects users to advertisers, and AirBnb connects homeowners to short-term renters. In this model, marginal ‘rents’ essentially become pure profit once a certain tipping point (critical mass) in market penetration has been reached. But more importantly, the path to this penetration is in theory, both straightforward and self-fulfilling. Metcalfe’s Law states that the value of a network grows exponentially even when the number of nodes grows linearly. In this sense, the company’s foundational competitive resource, is its growth!

None of this is particularly groundbreaking, but the important consideration is the shift in ‘scarcity’.

In orthodox economics, the sources of scarcity are internal resource-based constraints which force firms to make strategic choices on how they best want to win. In digital economics, scarcity is external. What’s difficult in digital networks is not the ability to disseminate or even create a service — the march to the asymptotic free deems all facets of that distribution virtually costless. Uber doesn’t have to make resource-based strategic choices on its market positioning like a physical car manufacturer would. Uber offers both luxury and mid-tier services — UberBlack and UberX — and its ability to offer unique services to disparate segments comes at no additional marginal cost. Facebook doesn’t have to set up new manufacturing and distribution facilities when it wants to roll out a new feature like Instant Articles.

Thus, the ‘constraint’ or difficulty lies not in production but in incentivising a sufficient number of nodes to participate to make a network worthwhile. To that end, what is scarce is now consumer’s time and attention and not our capacity to produce.

Evidently, the theory of comparative advantage now leaves something to be desired. When it is almost free to pursue any strategic possibility, choices no longer need to be made on the basis of comparative advantage. A digital firm is free to employ any combination of once mutually exclusive generic strategies, for example differentiation and cost leadership in tandem. As such, the resultant competitive landscape tends to be significantly less diverse. Successful digital firms naturally gravitate towards monopoly market share, where value for customers or ‘nodes’ is greatest.

The Production Possibility Frontier as a concept ceases to exist in the realm of digital goods since marginal production and distribution is costless. Uber doesn’t have to choose how many UberX’s and UberBlack’s it has on the streets at any time, the production capacities of both are theoretically infinite, bound only by the external factor of the number of nodes in Uber’s network. Is there such a thing as Pareto optimality in production scenarios that are entirely unbounded? It wouldn’t make sense.

So in a world where production constraints don’t exist, consumption constraints must. With infinite supply, there is a finite capacity to consume — consumers only have so much time, and so much attention to give. What we’re really concerned with here is a Consumption Possibility Frontier: what is the optimal combination or bucket of goods that consumers should consume to obtain the greatest surplus? Now that scarcity has moved from an internal constraint to an external constraint, so does the burden of choice.

To what end?

These are conversations worth having. This story hasn’t sought to introduce a new model, but simply to spark some introspection into the digital trends that are becoming more pedestrian than they are radical. Considering new economic models that explain optimal managerial decision making in the world of digital networks may provide some guidance into how we optimise the welfare of firms, but also customers, and how they choose to use things.